Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

For more information on preparing to sell your home, visit my Home Selling Guide:

Sun’s out…fun’s out! Our glorious PNW summer is coming in hot with endless opportunities to enjoy the outdoors. Here are some fun and easy project ideas to help you make the most of it!

Outdoor movies are a great way to enjoy your yard and entertain a crowd (and keep the mess outside, too!). Looking for affordable and easy? You can find portable, outdoor, Bluetooth enabled projectors for under $100; hang up a white sheet or inexpensive screen, grab your portable Bluetooth speaker, and BOOM…it’s movie time. Ready to take the leap and create something more lasting? Here is a great how-to for a wooden frame with pull-down screen + helpful tips for your AV setup.

Who doesn’t love a good s’mores roast? Creating an attractive fire pit may be easier and cheaper than you imagined. One beautifully simple method we love is to create a ring of stacked bricks, stones or cinder blocks on top of a level pea gravel base, then place a store-bought metal fireplace bowl in the center (here is the full how-to). It’s remarkably fast and you don’t even need mortar! You can also go for a modern square look with cinder blocks, use a reclaimed metal receptacle, or find a full kit at the hardware store. Check out this list of 31 DIY fire pit ideas from the Spruce.

Looking to add some instant curb appeal to your home? This elegant, inexpensive design may just be the “WOW!” you’re looking for. Choose modern house numbers for an updated look and then a little wood, some pretty plants, and a couple hours of work is all it takes to make your neighbors jealous.

Photo courtesy of ana-white.com

We LOVE this idea for summer BBQs, and it’s so easy! All you need are some 2×3 boards, a miter saw, and sandpaper (or a power sander, if you have one). Bada bing bada boom…jumbo Jenga to entertain kids and adults alike. Here are full instructions courtesy of Her Tool Belt, including the option to go fancy with colors and a DIY carrying crate that also doubles as a stand.

If you’re lucky enough to have central A/C, you’re also unlucky enough to have an unsightly metal unit sitting in your yard. Fortunately, you can build a simple cover for less than $100 and in less than a day. Here is an easy plan from This Old House, designed with widely spaced slats for air flow and 1 foot of clearance (do your homework on your specific A/C unit before you dive in—you may need to size up). You can paint it to match your house color if you want to go incognito, or stain it for a stylish natural wood look.

Photo courtesy of tarynwhiteaker.com

Taking advantage of vertical space for planting means that even the smallest of patios can host a garden. It could be as simple as attaching pots to a trellis/rail or framed chicken wire, or something more elaborate like this beautiful living wall by This Old House. Vertical gardens can also double as privacy screens for your yard, porch or patio. Veggie enthusiasts can even build this easy vertical ladder planter with its own drip watering system. For the ultimate quick fix, felt pocket planters offer instant gratification—just attach to your fence or wall, add potting soil + slow release fertilizer + drought-tolerant plants, and water every 2 days. Using freestanding shelves for your container garden is another great option, especially for tenants who need something that is easily removable.

We love conservationist Aldo Leopold’s simple and iconic wooden bench plan, designed to be used both forward (with a backrest) or backward (where the backrest becomes an elbow rest for using binoculars). Here is a super easy DIY plan with cutting instructions from Construct101. Even amateurs can build this in less than a day, and all it takes are three boards, 6 carriage bolts, and some screws!

Photo courtesy of etsy.com

This ingenious project will boost your curb appeal in two ways, both by being an attractive planter AND by stowing away unsightly hoses in a clever hidden storage compartment. There are a few different styles and plans out there. We like this version from DIY Candy with a hinged front that allows you to access the hose without having to lift up the heavy planter. It can be crafted from a pallet or any other reclaimed wood. The Kim Six Fix also has this version made with cedar fence boards instead.

Photo courtesy of diycandy.com

Did the April showers leave your yard (or basement) a little soggy? Sump pump working overtime? A rain garden is a beautiful way to channel water away from your house while also helping the environment by keeping chemical runoff out of rivers and lakes. The concept is pretty simple: create a below-grade garden bed planted with deep-rooted species that help capture and drain water rapidly into the soil. If you’re serious about improving drainage, you’ll also want either a stone channel or buried PVC pipe to help guide water from your downspout into the garden. Collect some friends to help with the digging! Here are full instructions from the Family Handyman.

If you’re considering selling your home, some of these projects—like planters and vertical garden privacy screens—can help maximize your curb appeal. A rain garden might also be a beautiful solution for drainage issues that need to be resolved before your house can go on the market. Looking for more ideas or advice? Reach out to me any time…I’m never too busy to help!

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2024, Windermere Real Estate/Mercer Island.

In today’s rapidly changing real estate landscape, understanding the critical role of buyer representation has never been more essential for home sellers. With the pending NAR settlement on the horizon, many sellers may not fully grasp the significant impact these changes will have on their transactions. The urgency to adapt is real, and overlooking the necessity of paying a buyer agent compensation could expose sellers to unforeseen risks.

Currently, home buyers are not allowed to roll their buyer agent compensation into their loan. This means they must bring cash to the table to pay their agent (if the seller is not offering buyer agent compensation).

Unrepresented buyers should be considered more than a minor hiccup—it can lead to a cascade of complications that jeopardize the entire deal. To safeguard your investment and ensure a smooth transaction, it’s crucial to recognize the invaluable support a buyer’s agent provides.

What value does a seller receive if the buyer has professional representation? Let us list the ways:

Lender Connections: Buyer agents connect their buyers with well-vetted (and typically local) lender partners who have proven time and again that they can close a transaction, and on time.

Documentation Management: Buyer agents ensure that buyers have delivered all necessary documentation to the lender to ensure full underwriting.

Market Analysis: Buyer agents provide comparable market analysis reports (CMAs) to help buyers understand the market value of the home and support a reasonable offer price.

Contract Guidance: Buyer agents guide their clients through the purchase and sale agreement, ensuring that they understand the terms and conditions and their ability to fulfill their commitments.

Contingency Explanation: Buyer agents explain all contingencies to buyers, ensuring they understand the risks and rewards, especially when waiving contingencies.

Earnest Money Handling: Buyer agents ensure that earnest money funds are delivered to escrow on time.

Transaction Deadlines: Buyer agents ensure that their client and their lender observe and adhere to all deadlines to keep the transaction flowing smoothly and closing on time.

Inspection Access: Buyer agents provide access to home inspectors and help their buyers understand the reports. This is critical as most MLS associations require an agent to be present whenever a door is opened. If the buyer doesn’t have representation, the listing agent must give access, exposing them to inspection findings and forcing them to disclose on behalf of the seller.

Appraisal Assistance: Buyer agents give access to appraisers and typically provide reports of comparable properties to support the purchase price, ensuring the property appraises at value.

Negotiation Support: If the appraisal report comes in less than the purchase price, the buyer agent will help negotiate and collaborate with the listing agent to ensure a mutual agreement is reached by all parties.

Transaction Coordination: Most importantly, the buyer agent helps keep their client and all parties on track to ensure closing, and crucially, on time.

The value a buyer agent brings to the transaction is indispensable. Their expertise not only facilitates a smoother process but also protects all parties involved from potential pitfalls. By ensuring the buyer has professional representation, sellers can avoid significant risks and secure a successful transaction. In the evolving real estate market, investing in buyer agent compensation is a wise decision that benefits everyone involved.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

This article originally appeared on the Windermere blog on 5/29/24 & Inman News on 5/21/24.

When it’s time to sell a home, we all dream of a flawlessly executed transaction where everything goes smoothly and ends with a win-win for you and the buyer. Here are seven tips to help make that happen—and avoid surprise expenses along the way…

Making repairs to your home before you sell not only makes it more appealing to buyers, but it can also help you avoid the additional costs that can result from the buyer’s inspection. Disclosing any repairs that still need to be made will help you move smoothly to closing and avoid problems that could otherwise kill the deal. Consider conducting a pre-listing inspection to make sure everything is out in the open before you sell.

The key to selling your home quickly is to find the right buyers. To find the right buyers, your home must be correctly priced. I use a Comparative Market Analysis (CMA)—a thorough, data-backed examination of your home and how it compares to other listings in your area—to accurately price your home. Without an agent’s CMA, it’s easy for your home to be listed at the wrong price.

First impressions matter when selling a home. The vast majority of buyers are searching online and taking virtual tours of homes they’re interested in. As such, it’s well worth the time and money to hire a high-quality photographer and I always provide this for my sellers. The right photography can make all the difference in the minds of buyers.

Home staging is also a critical element for getting the most value for a home and selling it quickly. You can even DIY if you have the time and modern decor. It’s also the perfect time to inspect your home for any minor or cosmetic repairs that can be addressed quickly. An aesthetically pleasing home will attract more eyes, and any edge you can give your home over competing listings may be just the ticket to getting it sold.

Selling your home is an act of learning how to let it go. Once you know you’re ready to sell, you’ll need to be able to look at it with an objective eye. This will allow you to approach decisions from a neutral standpoint and work towards what is best for the sale of the home. Having clear judgement will also help you get through the negotiating process and steer yourself toward a smooth closing. Stepping back can be tough, but a good agent will always be happy to give you guidance and help you keep perspective.

It may be tempting to rush your listing to take advantage of local market conditions, but waiting until you have all your ducks in a row will make life so much easier. Knowing when to sell your home is a mixture of being financially prepared, having the right agent, and understanding how your home fits into the current local market landscape. Once you’re ready, here are some tips on timing the market.

…and I’m not just saying it because I’m an agent! Selling a home “For Sale By Owner” (FSBO) can save on commission fees, but is a complex and risky process that can easily lead to serious costs. An agent will help you front marketing costs, provide sound advice to help you avoid legal trouble, and ultimately shoulder some of the liability for the transaction. Being represented by an experienced professional will help you avoid mistakes during the offer process, negotiations, and closing that could otherwise be costly or jeopardize the sale. It’s no wonder that a vast majority of sellers choose to work with an agent.

Approaching buyers’ offers with an open mind will ensure you don’t miss any opportunities. Before the offers start to come in, it’s important to work with your agent to understand your expectations and strategize which terms and contingencies you’re willing to negotiate on. That way, you can quickly identify the right offer when it comes along. Showing a willingness to work with buyers will also keep them engaged and make sure you don’t leave potential deals on the table.

© Copyright 2023 Windermere Mercer Island.

Adapted from articles that originally appeared on the Windermere blog, November 22, 2021 & April 7, 2021, by Sandy Dodge.

Getting your home ready to sell can feel like a circus act. Without the right organization, juggling the countless moving parts involved in this stage of the selling process can take its toll. This is the perfect opportunity to create a checklist to keep yourself on track and within your budget. The following information will illuminate the key responsibilities you face as a homeowner as you prepare to hit the market.

We’ve included a comprehensive checklist below of the common tasks required to get your home ready to sell. It is also available as a downloadable pdf here:

This list of value-adding curb appeal projects will help to form buyers’ first impressions of your home and make your ever-important exterior listing photos stand out amongst the competition.

Not only will these interior projects get your house sparkling clean, but they’re also preparatory steps for staging your home and hosting open houses.

For more information on preparing to sell your home, visit my Home Selling Guide:

This article originally appeared on the Windermere blog June 29th, 2022. Written by: Sandy Dodge.

© Copyright 2023, Windermere Real Estate/Mercer Island.

The following analysis of select counties of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. I hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact me.

Regional Economic Overview

Although the job market in Western Washington continues to grow, the pace has started to slow. The region added over 91,000 new jobs during the past year, but the 12-month growth rate is now below 100,000, a level we have not seen since the start of the post-COVID job recovery. That said, all but three counties have recovered completely from their pandemic job losses and total regional employment is up more than 52,000 jobs. The regional unemployment rate in November was 3.8%, which was marginally above the 3.7% level of a year ago. Many business owners across the country are pondering whether we are likely to enter a recession this year. As a result, it’s very possible that they will start to slow their expansion in anticipation of an economic contraction.

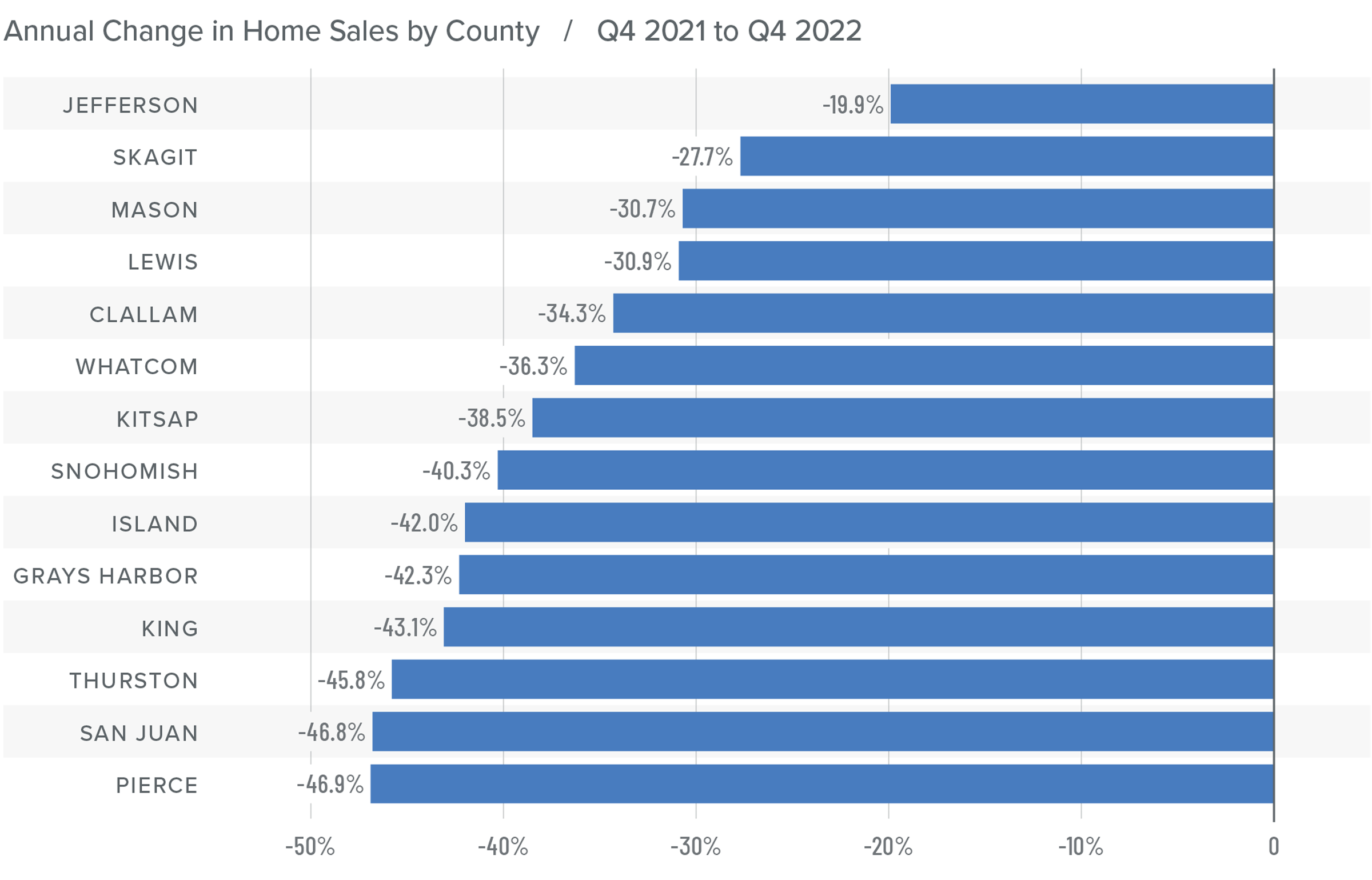

❱ In the final quarter of 2022, 12,711 homes sold, representing a drop of 42% from the same period in 2021. Sales were 34.7% lower than in the third quarter of 2022.

❱ Listing activity rose in every market year over year but fell more than 26% compared to the third quarter, which is expected given the time of year.

❱ Home sales fell across the board relative to the fourth quarter of 2021 and the third quarter of 2022.

❱ Pending sales (demand) outpaced listings (supply) by a factor of 1:2. This was down from 1:6 in the third quarter. That ratio has been trending lower for the past year, which suggests that buyers are being more cautious and may be waiting for mortgage rates to drop.

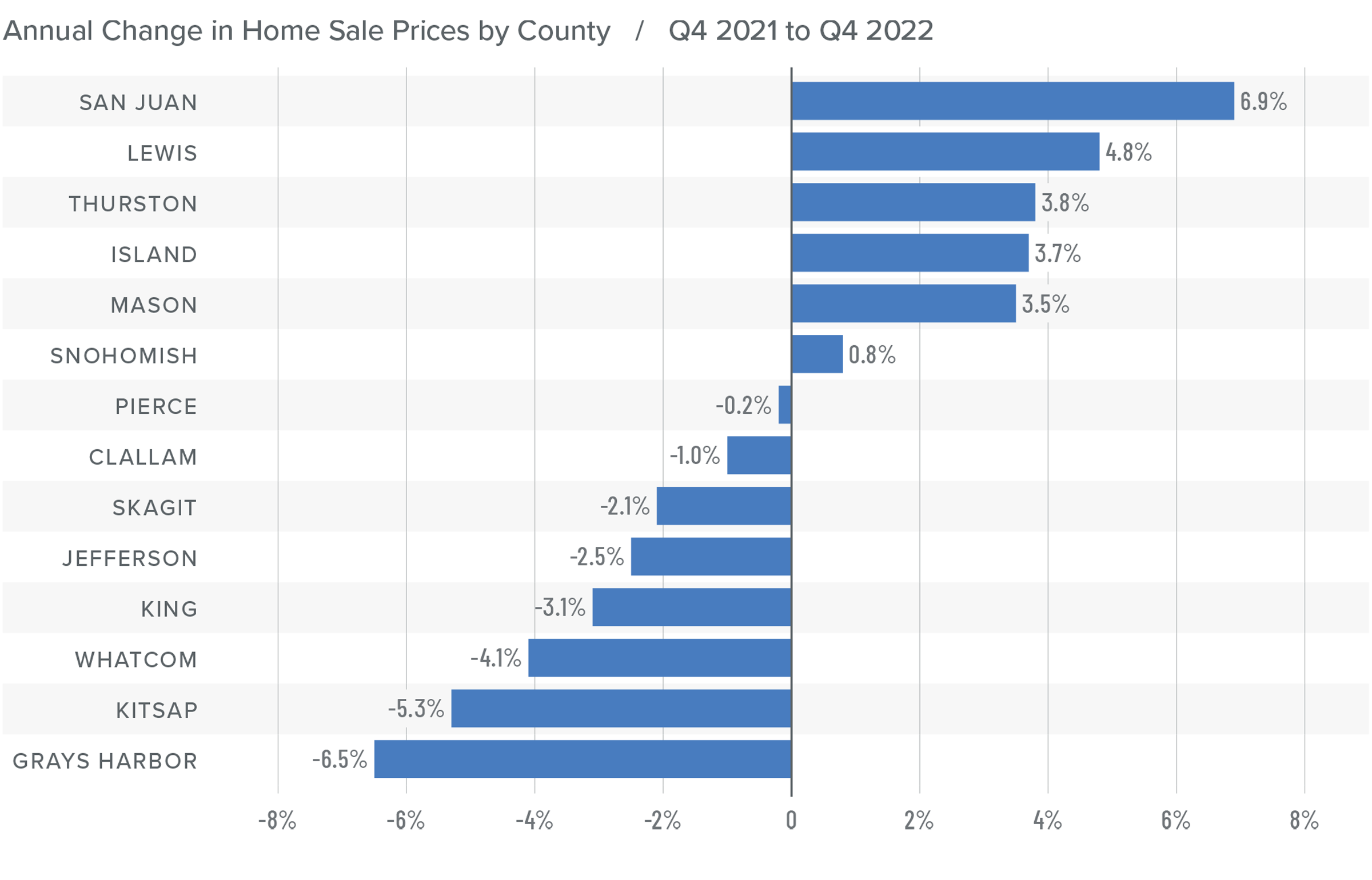

❱ Sale prices fell an average of 2% compared to the same period the year prior and were 6.1% lower than in the third quarter of 2022. The average sale price was $702,653.

❱ The median listing price in the fourth quarter of 2022 was 5% lower than in the third quarter. Only Skagit County experienced higher asking prices. Clearly, sellers are starting to be more realistic about the shift in the market.

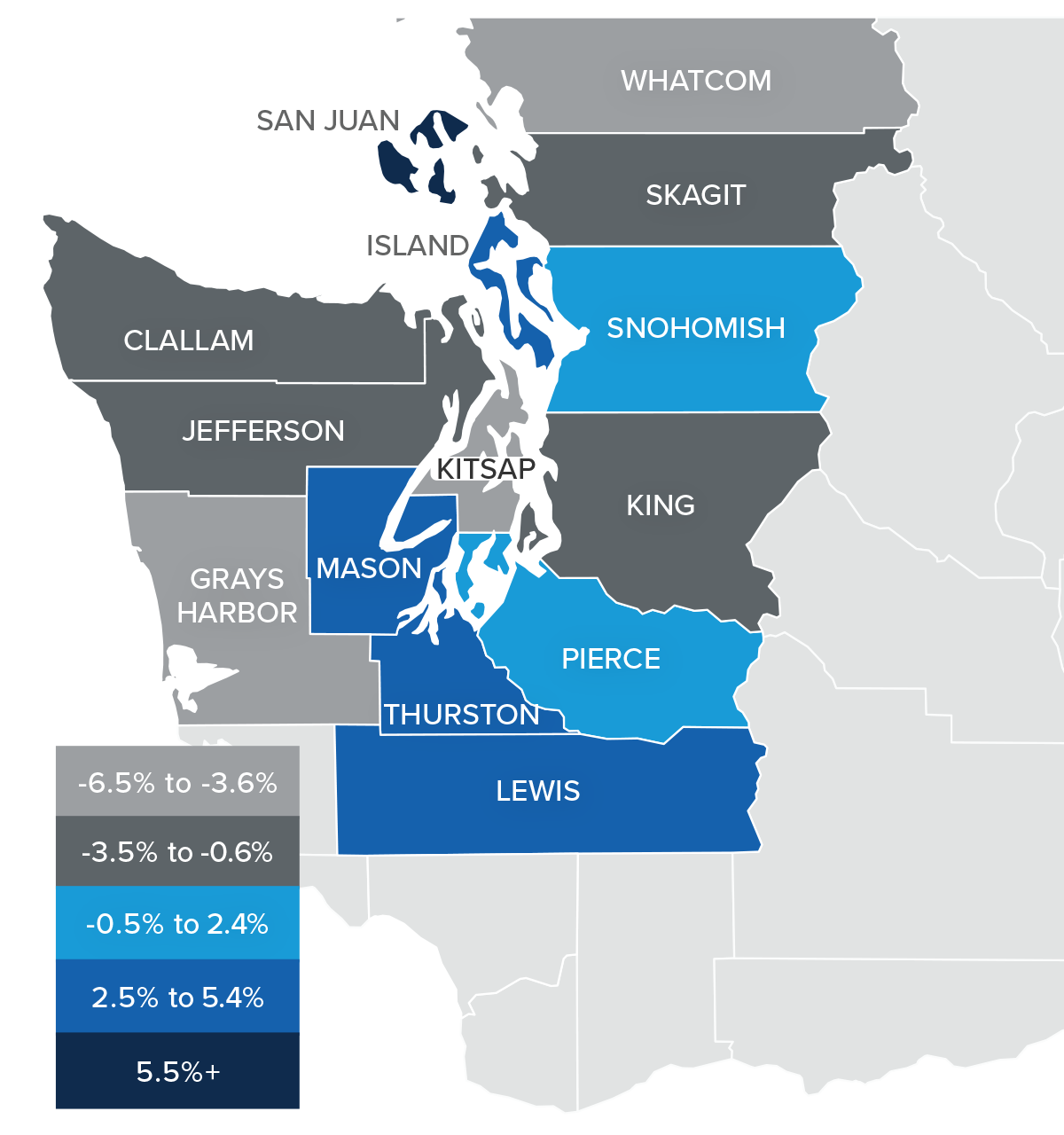

❱ Even though the region saw aggregate prices fall, prices rose in six counties year over year.

❱ Much will be said about the drop in prices, but I am not overly concerned. Like most of the country, the Western Washington market went through a period of artificially low borrowing costs, which caused home values to soar. But now prices are trending back to more normalized levels, which I believe is a good thing.

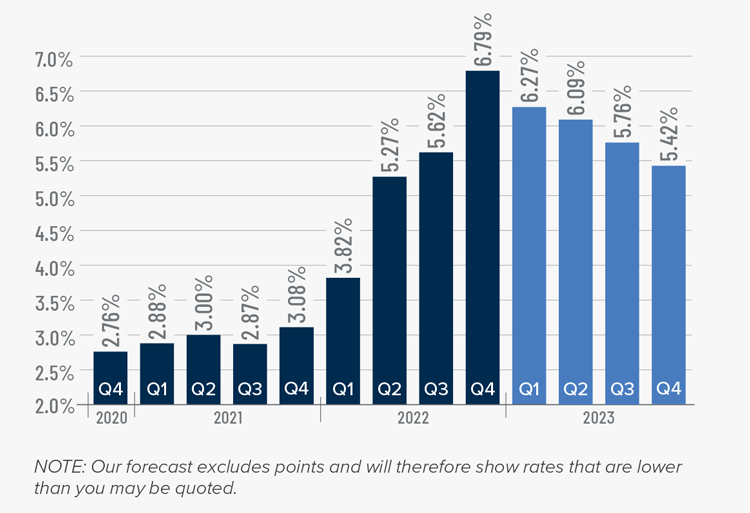

Rates rose dramatically in 2022, but I believe that they have now peaked. Mortgage rates are primarily based on the prices and yields of bonds, and while bonds take cues from several places, they are always impacted by inflation and the economy at large. If inflation continues to fall, as I expect it will, rates will continue to drop.

My current forecast is that mortgage rates will trend lower as we move through the year. While this may be good news for home buyers, rates will still be higher than they have become accustomed to. Even as the cost of borrowing falls, home prices in expensive markets such as Western Washington will probably fall a bit more to compensate for rates that will likely hold above 6% until early summer.

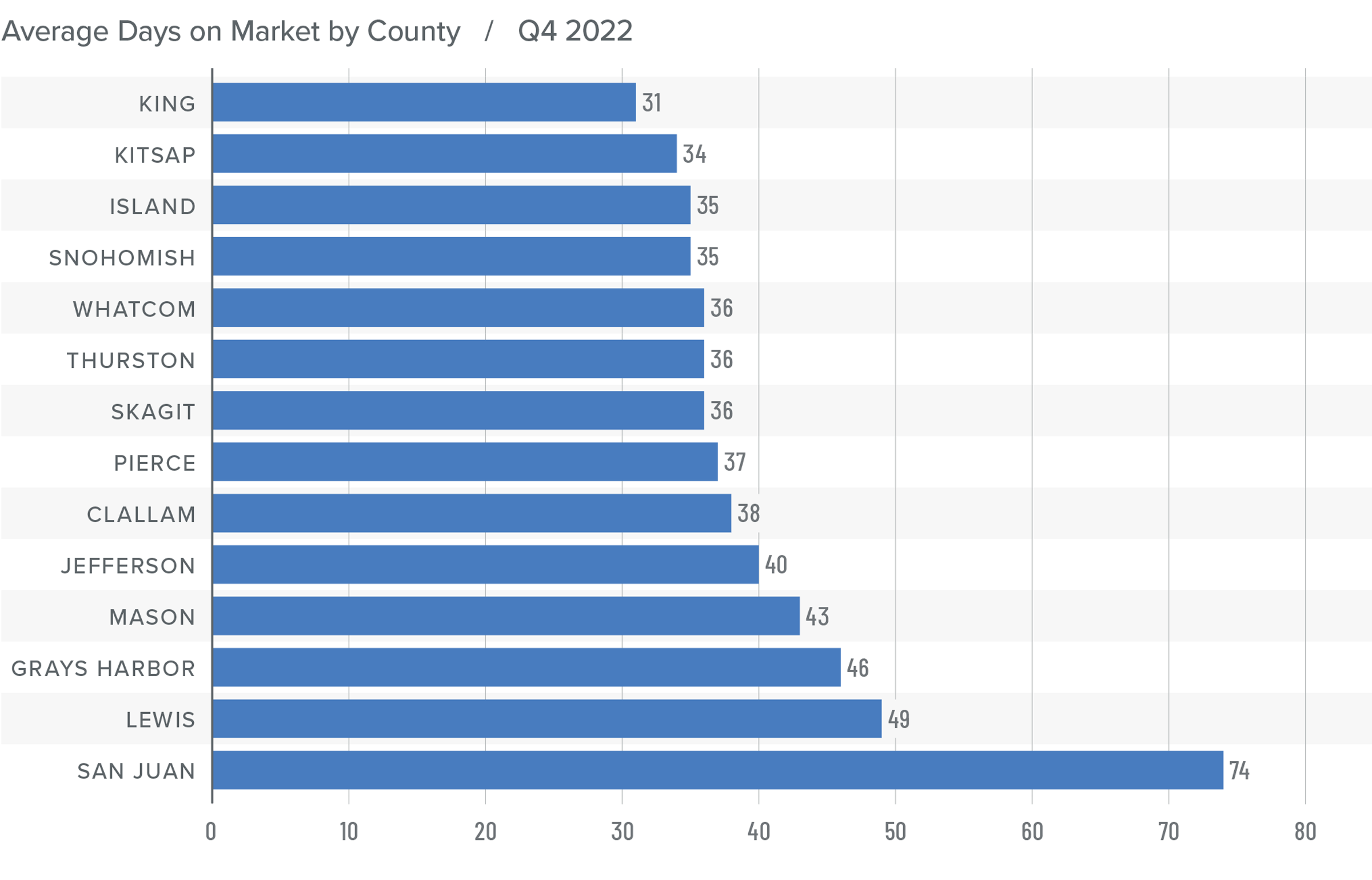

❱ It took an average of 41 days for homes to sell in the fourth quarter of 2022. This was 17 more days than in the same quarter of 2021, and 16 days more than in the third quarter of 2022.

❱ King County was again the tightest market in Western Washington, with homes taking an average of 31 days to find a buyer.

❱ All counties contained in this report saw the average time on market rise from the same period a year ago.

❱ Year over year, the greatest increase in market time was Snohomish County, where it took an average of 23 more days to find a buyer. Compared to the third quarter of 2022, San Juan County saw average market time rise the most (from 34 to 74 days).

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

The regional economy is still growing, but it is showing signs of slowing. Although this is not an immediate concern, if employees start to worry about job security, they may decide to wait before making the decision to buy or sell a home. As we move through the spring I believe the market will be fairly soft, but I would caution buyers who think conditions are completely shifting in their direction. Due to the large number of homeowners who have a mortgage at 3% or lower, I simply don’t believe the market will become oversupplied with inventory, which will keep home values from dropping too significantly.

Ultimately, however, the market will benefit buyers more than sellers, at least for the time being. As such, I have moved the needle as close to the balance line as we have seen in a very long time.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

This article originally appeared on the Windermere blog January 26th, 2023. Written by: Matthew Gardner.

© Copyright 2023, Windermere Real Estate/Mercer Island.

Securing the most advantageous financing for your situation is an integral part of the success formula of buying a home. After getting pre-approved but once you’ve found the home you’d like to pursue, one of your primary tasks is exploring different loan products to see which best fits your situation. This is the fork in the road where you’ll need to decide between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). The following information will help you gain a better understanding of ARMs to help you decide whether they’re right for you.

After your down payment, your mortgage will finance the remainder of your home purchase. Whereas fixed-rate mortgages allow you to lock in a specific interest rate and payment for the life of your loan, adjustable-rate mortgages’ interest rates will fluctuate over time, thus changing your loan payment. It’s typical for ARMs to begin with a low introductory interest rate, but once that first stage of the loan has passed, they will begin to shift up and down. ARMs generally have a cap that specifies the maximum rate that can occur for that loan.

Let’s say you secure an adjustable-rate mortgage with 30-year terms, the first five of which are at a fixed rate. When the variable interest portion of the loan kicks in, your mortgage’s fluctuations will be measured against an index. If the index is higher than when you secured the loan, your rate and loan payment will go up—and vice versa. How often your ARM rates change depends on your agreement with your lender. Talk to your mortgage broker to learn more about the characteristics of adjustable-rate mortgages.

| Pros | Cons |

|

|

|

|

|

|

|

Hybrid ARM: As outlined above, a hybrid ARM begins with a fixed-rate introductory period followed by an adjustable-rate period. Typically, a hybrid ARM’s fixed-rate period lasts anywhere between three to 10 years, and its rates adjust at an agreed-upon frequency during the adjustable-rate period, such as once every six months or once a year.

Interest-Only ARM: With an interest-only ARM, you pay just the interest on the loan for a specified introductory period, then the principal payments kick in on top. The longer the introductory period, the higher your payments will be when the delayed principal payments enter the equation.

Payment-Option ARM: Not all states allow these loan products because they can get home buyers into hot water quickly if rates increase. They include flexibility to choose your monthly payments with a payment-option ARM, including interest-only payments and minimum payments that don’t cover interest.

To get an idea of how your mortgage payment will fit into your budget, use our free Home Monthly Payment Calculator by clicking the button below. With current rates based on national averages and customizable mortgage terms, you can experiment with different values to get an estimate of your monthly payment for any listing price.

Adapted from an article that originally appeared on the Windermere blog September 28, 2022. Written by: Sandy Dodge.

© Copyright 2022, Windermere Real Estate/Mercer Island.

A clever person solves a problem;

a wise person avoids it.

As the days shorten, you can mitigate many mid-winter headaches with some preemptive prep. Proper weatherizing can help protect your home from preventable damage, save money on energy costs, and, most importantly, keep you and your loved ones safe and warm throughout the winter season. Here is a useful checklist to manage your weatherization project. Setting aside some time on a couple of weekend days should be more than enough to knock this out. Scroll down for helpful tips and click here for a printable checklist!

After all the leaves, pine cones, pine needles, and other autumnal debris have fallen, clear them out from your rain gutters. This will avoid gutter damage from ice or melted snow draining improperly. Even in warmer locales, gutter buildup & leakage can put undue stress on your roof and home. Make sure your downspouts are pointing away from your home’s foundation to prevent basement leaks and flooding.

Check for any damaged shingles, corroded flashing, or leaky vents that need to be repaired. When the first heavy rain comes after a long dry spell, check the underside of the roof for moisture on joints or insulation. Mark any spots that you find and then hire a roofing specialist to repair these leaks. If you wait until spots show up on your ceiling, insulation and sheet rock will have also been damaged and you could have a mold problem too. You can find tips on how to solve roof & gutter issues in this great article from http://FamilyHandyman.com.

While the weather is still nice, look for any gaps or cracks and seal them with exterior caulk (here are some tips). You should also touch up any old or loose paint to ensure your home’s exterior has a weatherproof seal.

If your property has large trees, check for loose branches and call someone to trim back any limbs that may fall in your yard, on your roof or even damage a window. Branches that touch your house and overhang your roof are convenient on-ramps for pests, so trim back branches so they’re at least four feet from the house.

If you have ceilings fans in your home, there is a handy trick you can use to improve your home’s heating efficiency. By reversing the direction of your ceiling fan—running the blades in a clockwise direction—you’ll create a slight updraft, forcing warm air near the ceiling downward.

If an exterior door doesn’t have a snug seal when closed, replace the weather stripping; self-adhesive foam stripping is much simpler to install than traditional vinyl stripping but has a shorter lifespan. If there is a gap under the door (which can happen over time as a house settles), you may need to realign the door and replace the vinyl door bottom and/or door sweep.

Preventative maintenance is crucial for your home’s heating and air-conditioning systems. Fall is a smart time to have your systems checked and tuned up. Don’t wait for extreme temperatures to arrive, when service companies are slammed with emergency calls. Replace filters if you use a furnace and clear out any vents and ducts that carry heat through them. If you have baseboard heaters, wipe them of dust and remove any debris that might catch fire.

Make sure to have chimneys and air vents inspected and cleaned early in the season if you are planning on warming your home with a wood-burning source. When your fireplace is not in use, make sure to close the damper—some resources estimate an open damper can increase energy consumption by as much as 30%, increasing your bill about $200.

Most house fires happen in the fall and winter, with holiday cooking and heating systems both being common causes. Deadly carbon monoxide can also be released by furnaces, stoves, fireplaces, and space heaters. Protect your household by replacing any smoke detectors and carbon monoxide monitors as needed. Check the indicators on your fire extinguishers to make sure they’re still good (or install them if you don’t have them—a Class B extinguisher for the kitchen is a good place to start, but you might need more according to this guide).

Make sure any pipes in unheated spaces—such as the crawl space, basement, or garage—are properly insulated to prevent freezing and bursts. Disconnect hoses and install hose bib covers on all outdoor faucets. Winterize your in-ground sprinkler system…here’s a great wikiHow article with 3 different methods.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2022 Windermere Mercer Island.

Adapted from articles that originally appeared on the Windermere blog December 21, 2020, by Sandy Dodge; October 7th, 2019 by Meaghan McGlynn; and September 16, 2016 by Windermere Staff.

Here are four home attributes beyond the number of bedrooms and baths that you should have your eye on…

Home (building) quality: Very well-built homes are a rare find and typically worth every penny of their price. Don’t confuse them with so-so homes that just measure up to the city inspector’s threshold. Lesser quality homes will cost you more in upkeep and replacement as systems and components wear out. If you purchase a lesser quality home for less, the differential might just cover the added maintenance expense. But, if you purchase a fair quality home at the going rate of higher quality homes, you might likely be overpaying.

Deferred maintenance: Different than home quality, deferred maintenance includes the to-do list of items that need to be done to maintain a home’s integrity. A home that has been well maintained over its life typically is a better investment than one that hasn’t. The true cost of deferred maintenance often adds up to more than the cost of the repairs themselves. Don’t forget to factor in the reduced life span of other components—like replacement of damaged wood beneath peeling paint or mold remediation in a damp basement caused by a clogged foundation drain.

Setting: The saying “location, location, location” didn’t get its fame from out of nowhere. A home with an ideal setting on its lot and in the neighborhood—away from busy roads and utility poles/boxes, with adequate privacy, good topography, best positioned to capture views if available, and not adjacent to undesirable elements (poorly maintained homes, water towers or other unsightly public structures, high traffic facilities, etc.) will have more value than a less-ideally sited home. When deciding what to pay for a property it is critical that you evaluate these aspects and any others relevant to a specific neighborhood to determine the +/- effect on value.

Floor plan: How a home lives—flow from room to room, size of rooms, open/closed-off spaces, and below ground vs. above ground living are every bit as important as the total home square footage. You can change a lot of things about a home, but it is very difficult to change a bad floor plan. When you are deciding how high to make that multiple offer bid, consider factoring in the added value or take-away of the floor plan.

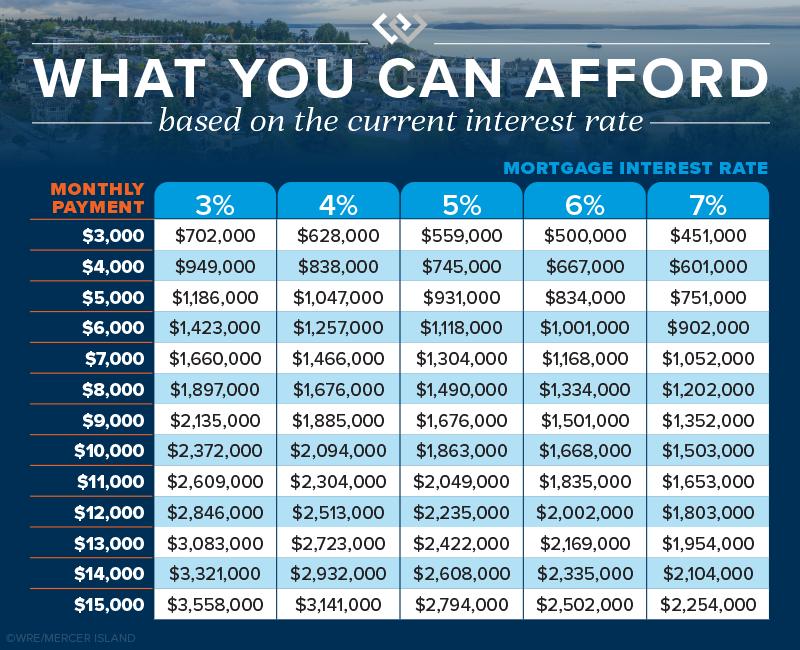

Interest Rates: In addition to being more selective about the home itself, it pays off to understand how interest rates impact your monthly housing cost. It’s a bigger deal than you might think. Every 1% increase in interest rate equates to roughly a 10% decrease in buying power. Said differently, a 10% drop in home sale price would be wiped out by a subtle 1% increase in mortgage interest rate. This means you can obtain a much more expensive home when rates are low, whereas higher rates get you less home—even though you still pay the same monthly payment.

If you have $5,000 a month to budget for a house payment (before taxes and insurance), you could purchase a $931,000 house at a 5% mortgage rate. If rates went up to 6%, the same monthly payment would only get you an $834,000 home. Your buying power diminishes considerably with each bump up in rates.

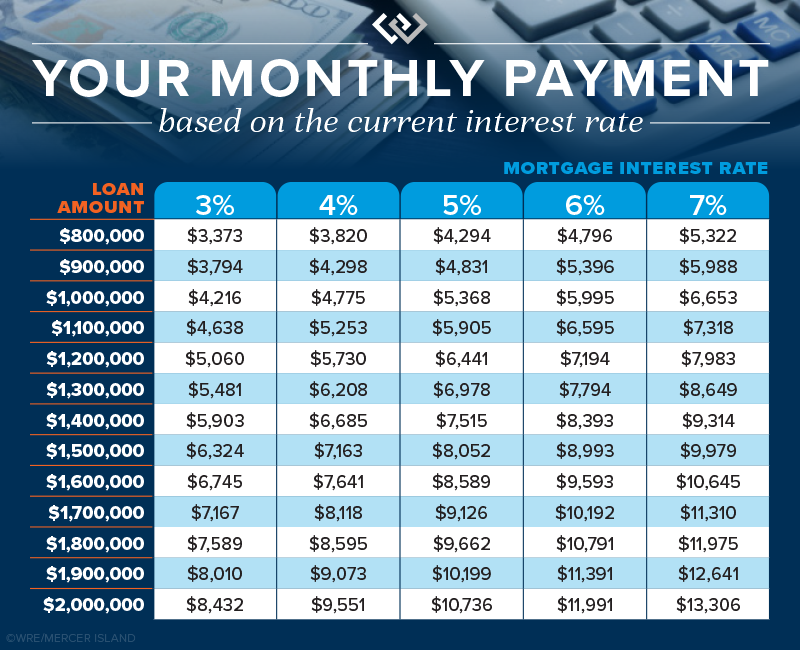

This second chart below shows how interest rates impact monthly payments. If you’re purchasing a $950,000 house at a 5% interest rate, you’ll be paying $596 less every month than if rates were 6%. That adds up quick…$7,152 in one year alone!

Job and Location Stability: Like nearly any investment vehicle, being able to buy and sell on your own time allows you take advantage of ideal market conditions or hold until a more favorable market returns. In an uncertain market, you should plan to be able to stay put for a minimum of 5-7 years if needed. If relocation or job loss is a distinct possibility, waiting to buy might avoid loss as a result of an untimely sale.

Homeownership Lifestyle: For many, homeownership represents a life accomplishment, independence, and financial security. For others, one more thing requiring maintenance and upkeep. Knowing where you stand (at this moment in time anyway) when it comes to evaluating the pros and cons of homeownership as a lifestyle choice is a better first step than an afterthought.

Want to know how you can best protect yourself in a changing real estate market? Reach out to us for help evaluating whether it would make financial sense to buy now or wait.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2022, Windermere Real Estate/Mercer Island.

© Windermere Real Estate