Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Planning Ahead: A 12-Month Guide to Buying Your First Home

Thinking about buying a home can be daunting, especially if it’s your first time. What should be an exciting milestone can feel overwhelming without a clearly defined roadmap, and diving in headfirst without a solid plan can lead to unnecessary stress, financial surprises, and missed opportunities. However, by establishing a timeline and breaking the process down into manageable steps, you can move forward with confidence and clarity.

Here is your month-by-month guide to preparing for a successful home purchase in the following year.

12 – 10 MONTHS OUT

Know Your “Why”

Understand your motivation for buying. Are you relocating, growing your household, or ready to invest in your future? Clearly defining your “why” will help shape your search criteria and influence your budget, location, and timeline.

Set Clear Goals

Start to think about what you want in your new home. Create a list of your wants versus must-haves, including location, budget, size, and style of home. These goals will act as a compass throughout your search. Be sure to include your ideal timeline and what you hope to get out of the overall experience.

Find an Agent Who Prioritizes Your Goals and Timeline

A trusted real estate agent is more than just a facilitator; they’re a guide, negotiator, and advocate. Look for someone who understands your timeline and long-term vision and is familiar with the local market. Ask them to provide a first-time buyer’s guide or checklist to help you get started. Building this relationship early allows your agent to understand your needs and preferences in advance, setting the stage for a smoother process when you’re ready to make your move.

9 – 7 MONTHS OUT

Assess Your Finances

Take a close look at your income, debt, and spending habits. Use this time to create a monthly budget that includes future mortgage payments, utilities, insurance, taxes, and home maintenance. Many experts recommend spending no more than 28% of your gross monthly income on housing costs.

Boost Your Credit

Your credit score has a significant impact on your buying power, including your mortgage rate and loan approval. Take the next few months to pay down high-interest debt, stay current on all payments, and avoid opening new credit accounts. Check your credit report for errors and work on improving your score if needed.

Start Saving

You’ll want to have enough set aside not only for a down payment, which is typically 3% to 20% of the purchase price, but also for closing costs, moving expenses, and initial home repairs or furnishings. During this time, try to avoid nonessential major purchases and think about setting up a dedicated home savings account to stay consistent.

6 – 4 MONTHS OUT

Talk to a Financial Advisor

A financial advisor can help you align your financial goals with your homebuying plans. They can offer advice on what you can realistically afford and help identify areas to strengthen your financial readiness. You can also use tools like an online mortgage calculator to get a clearer idea of what your future monthly payments might look like.

Research Homebuyer’s Courses & Guides

Take advantage of first-time homebuyer resources, guides, and online courses. The more you know earlier on, the more confident you’ll feel.

3 – 2 MONTHS OUT

Familiarize Yourself with the Market

Start browsing homes and monitoring prices in the neighborhoods you’re interested in. Learn whether your local market is currently favoring buyers or sellers and what that could mean for your strategy.

Meet with a Lender and Get Pre-Approved

Meeting with a lender and getting pre-approved can help give you a clear picture of how much you can borrow and what price range to shop within. It also shows sellers that you’re a serious buyer when the time comes to make an offer. Your realtor can recommend trusted lenders to work with and assist you through this process.

Start Your Home Search

Now that you have your list of wants and needs and know your price range, you’re ready to start searching for your dream home. Use online property research tools to filter by location, features, and price to see what’s available in the locations you like. Narrow down your top homes and start scheduling showings and comparing listings.

1 MONTH OUT

Make an Offer

Once you find “the one,” your agent will help you craft a competitive offer, negotiate terms, and guide you through contingencies.

Get a Home Inspection

If your offer is accepted, a licensed inspector will identify any issues with the property before you finalize your purchase. Depending on what comes up, this can give you leverage to negotiate repairs or price adjustments.

THE TIME HAS COME

Closing On Your New Home

You’ve made it! During closing, you’ll sign paperwork, pay final costs, and receive the keys to your new home. Your agent and lender will walk you through the final steps to ensure everything goes smoothly.

Buying a home may seem like a big leap, but with a solid 12-month plan and the right support, it can be an extremely rewarding experience. Take it one step at a time and know that I’m here to help whenever you’re ready.

This article originally appeared on the Windermere Blog

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2026, Windermere Real Estate/Mercer Island.

A Consumer’s Guide to Homeowners Insurance

If you’re a homeowner or looking to buy a home, insuring your property is critical to protecting your investment—and if you’re getting a mortgage, it’s a must. It can be daunting trying to navigate the many options available to you. What does your policy cover…and what isn’t covered? What does the insurance company provide if your property is damaged or destroyed? Recently, the National Association of REALTORS® released this helpful guide on understanding the ins and outs of homeowners insurance. Here is a quick rundown of what you need to know…

How does property insurance work?

For certain unexpected events that cause a loss to your home or property, homeowner’s insurance can cover the cost to repair/rebuild the property and other structures like fences or garages. Most policies also cover personal belongings within the home, legal/medical fees for accidents occurring on the property, and temporary housing if a covered event (like a house fire) makes your home uninhabitable.

What losses are covered?

Your insurance policy will list the specific “perils” that are covered. The most common type of policy covers both the structure and personal assets for losses from house fires, storms, freezing, theft, vandalism, and sudden plumbing bursts—this is known as a HO-3 or “Special Form” policy. Most policies don’t cover earthquakes or natural floods (although you can get additional policies for those perils).

Is insurance required?

There are no laws requiring you to maintain homeowners insurance. However, most lenders require it for the duration of your mortgage. Required or not, it’s generally a good idea to protect your assets (especially if you have a lot of equity in your home).

What is the cost, and how is it paid?

As with many costs, insurance premiums are on the rise throughout the country (here’s how much, where, and why). Your individual policy’s cost will be based on your home’s age, size, condition, location, and other factors like whether you have a security system or have added on additional coverage. You may have the option to pay the premium annually or break it into smaller payments. If you have a mortgage, the lender usually collects a monthly “escrow” payment that they keep in an account to pay the insurance premiums and property taxes from on your behalf.

What happens in the event of a loss?

Most insurers will cover “replacement cost”—the amount needed to buy a new, comparable version of what you lost up to a dollar limit specified in the policy. It’s important to understand that replacement cost is not the same as market value; you’ll be compensated for the actual cost to repair/rebuild/replace your home regardless of what you paid for it or what you could sell it for. Typically the insurer will reimburse you to have your home repaired or replaced with comparable quality if it’s insured to at least 80% of it’s replacement cost, less any deductible that your policy has.

Alternatively, “actual cash value” is the current value of an item that depreciates over time or with use (often used for replacing personal or under-insured property). For example, if you paid $2,000 for your new couch but now it’s only worth $1,000 due to normal wear and tear, your insurer will only pay $1,000 less the deductible. You may choose to upgrade your personal property coverage to replacement cost instead for an extra fee.

For extra peace of mind, you can also purchase an extended replacement cost policy that provides extra coverage up to a set percentage above the policy limit. This can protect you if your home costs more than anticipated to rebuild.

Are the premiums tax deductible?

The short answer is no, unless you run a business from your home or it’s a rental property. However, you may be able to claim a casualty loss deduction if you suffered a loss due to a federally declared disaster (but check in with your tax pro for advice specific to your situation).

Because laws vary from state to state, it’s important to do your homework if you’re purchasing a home in an unfamiliar area. You can either connect with me or your attorney for advice.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2025, Windermere Real Estate/Mercer Island.

How to Avoid Overpaying for a Home in a Transitioning Market

Look Carefully at the Home Itself

Here are four home attributes beyond the number of bedrooms and baths that you should have your eye on…

Home (building) quality: Very well-built homes are a rare find and typically worth every penny of their price. Don’t confuse them with so-so homes that just measure up to the city inspector’s threshold. Lesser quality homes will cost you more in upkeep and replacement as systems and components wear out. If you purchase a lesser quality home for less, the differential might just cover the added maintenance expense. But, if you purchase a fair quality home at the going rate of higher quality homes, you might likely be overpaying.

Deferred maintenance: Different than home quality, deferred maintenance includes the to-do list of items that need to be done to maintain a home’s integrity. A home that has been well maintained over its life typically is a better investment than one that hasn’t. The true cost of deferred maintenance often adds up to more than the cost of the repairs themselves. Don’t forget to factor in the reduced life span of other components—like replacement of damaged wood beneath peeling paint or mold remediation in a damp basement caused by a clogged foundation drain.

Setting: The saying “location, location, location” didn’t get its fame from out of nowhere. A home with an ideal setting on its lot and in the neighborhood—away from busy roads and utility poles/boxes, with adequate privacy, good topography, best positioned to capture views if available, and not adjacent to undesirable elements (poorly maintained homes, water towers or other unsightly public structures, high traffic facilities, etc.) will have more value than a less-ideally sited home. When deciding what to pay for a property it is critical that you evaluate these aspects and any others relevant to a specific neighborhood to determine the +/- effect on value.

Floor plan: How a home lives—flow from room to room, size of rooms, open/closed-off spaces, and below ground vs. above ground living are every bit as important as the total home square footage. You can change a lot of things about a home, but it is very difficult to change a bad floor plan. When you are deciding how high to make that multiple offer bid, consider factoring in the added value or take-away of the floor plan.

Beyond the Four Walls

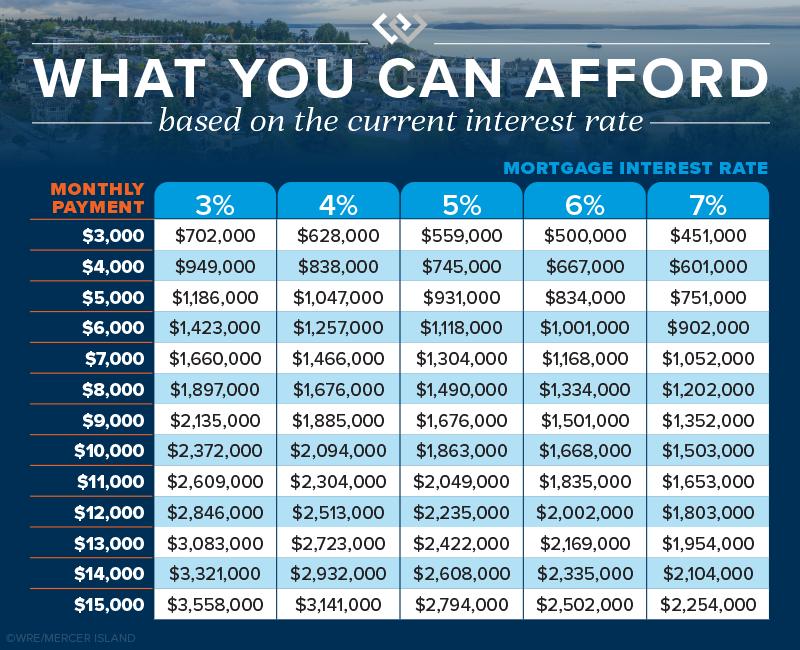

Interest Rates: In addition to being more selective about the home itself, it pays off to understand how interest rates impact your monthly housing cost. It’s a bigger deal than you might think. Every 1% increase in interest rate equates to roughly a 10% decrease in buying power. Said differently, a 10% drop in home sale price would be wiped out by a subtle 1% increase in mortgage interest rate. This means you can obtain a much more expensive home when rates are low, whereas higher rates get you less home—even though you still pay the same monthly payment.

If you have $5,000 a month to budget for a house payment (before taxes and insurance), you could purchase a $931,000 house at a 5% mortgage rate. If rates went up to 6%, the same monthly payment would only get you an $834,000 home. Your buying power diminishes considerably with each bump up in rates.

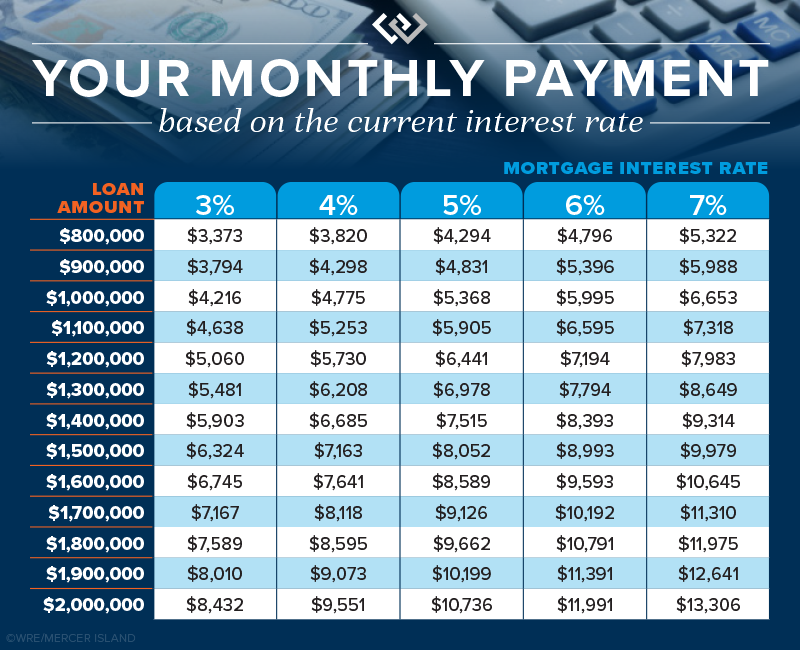

This second chart below shows how interest rates impact monthly payments. If you’re purchasing a $950,000 house at a 5% interest rate, you’ll be paying $596 less every month than if rates were 6%. That adds up quick…$7,152 in one year alone!

Job and Location Stability: Like nearly any investment vehicle, being able to buy and sell on your own time allows you take advantage of ideal market conditions or hold until a more favorable market returns. In an uncertain market, you should plan to be able to stay put for a minimum of 5-7 years if needed. If relocation or job loss is a distinct possibility, waiting to buy might avoid loss as a result of an untimely sale.

Homeownership Lifestyle: For many, homeownership represents a life accomplishment, independence, and financial security. For others, one more thing requiring maintenance and upkeep. Knowing where you stand (at this moment in time anyway) when it comes to evaluating the pros and cons of homeownership as a lifestyle choice is a better first step than an afterthought.

Final Thoughts

Want to know how you can best protect yourself in a changing real estate market? Reach out to us for help evaluating whether it would make financial sense to buy now or wait.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2022, Windermere Real Estate/Mercer Island.