Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Should You Remodel or Sell Your Home As Is?

Homeowners who are preparing to sell are often faced with a dilemma about whether to remodel or sell their home in its current state. Each approach has its respective advantages and disadvantages. If you decide to remodel your home, it will likely sell for more; but the increased selling price will come at the cost of financing the remodeling projects. If you decide to sell without remodeling, you won’t spend as much money putting your home on the market, but the concern is whether you’re leaving money on the table.

Should I Remodel or Sell My Home As Is?

To answer this question, it’s important to understand the factors that could influence your decision and to work closely with your agent throughout the process.

Cost Analysis: Home Remodel vs. Selling Your Home As Is

Home Remodel

When you remodel your home before selling, you’re basically making a commitment to spend money to make money. So, it’s important to consider the kind of ROI you can expect from different remodeling projects and how much money you’re willing to spend. Start by discussing these questions with your agent. They can provide you with information on what kinds of remodels other sellers in your area are making and the returns they’re seeing as a result of those upgrades. This will help you determine the price of your home once your remodel is complete.

Then, there’s the question of whether you can complete you remodeling projects DIY or if you’ll need to hire a contractor. If hiring a contractor seems expensive, know that those costs come with the assurance that they will perform quality work and that they have the skill required to complete highly technical projects.

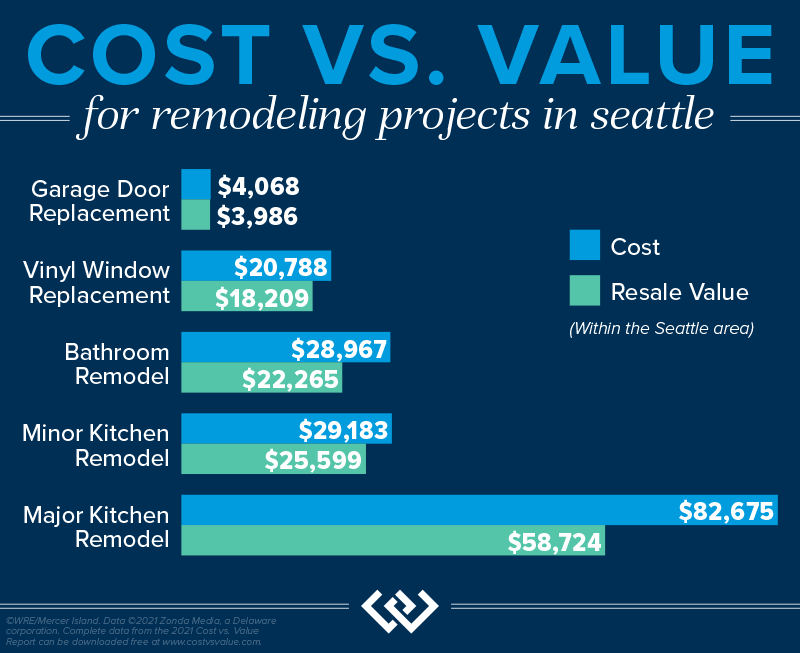

According to the Remodeling 2021 Cost vs. Value Report for Seattle (www.costvsvalue.com1), on average, Seattle-area homeowners paid $28,967 for a midrange bathroom remodel and $29,183 for a minor kitchen remodel, with a 76.9% and 87.7% ROI respectively. This data shows that, for these projects, you can recoup a chunk of your costs, but they may not be the most cost-effective for you. A more budget-friendly approach to upgrading these spaces may look like repainting your kitchen cabinets, swapping out your old kitchen backsplash for a new one, refinishing your bathroom tub, or installing a new showerhead. Other high-ROI remodeling projects may allow you to get more bang for your buck, such as a garage door replacement or installing stone veneer. To appeal to sustainable-minded buyers, consider these 5 Green Upgrades that Increase Your Home Value.

Selling Your Home As Is

Deciding not to remodel your home will come with its own pros and cons. By selling as is, you may sell your home for less, but you also won’t incur the cost and headache of dealing with a remodel. And since you’ve decided to sell, you won’t be able to enjoy the fruits of the remodel, anyway. If you sell your home without remodeling, you may forego the ability to pay down the costs of buying a new home with the extra money you would have made from making those upgrades.

Market Conditions: Home Remodel vs. Selling Your Home As Is

Local market conditions may influence your decision of whether to remodel before selling your home. If you live in a seller’s market, there will be high competition amongst buyers due to a lack of inventory. You may want to capitalize on the status of the market by selling before investing time in a remodel since prices are being driven up, anyway. If you take this approach, you’ll want to strategize with your agent, since your home may lack certain features that buyers can find in comparable listings. In a seller’s market, it is still important to make necessary repairs and to stage your home.

In a buyer’s market, there are more homes on the market than active buyers. If you live in a buyer’s market, you may be more inclined to remodel your home before selling to help it stand out amongst the competition.

Timing: Home Remodel vs. Selling Your Home As Is

Don’t forget that there is a third option: to wait. For all the number crunching and market analysis, it simply may not be the right time to sell your home. Knowing that you’ll sell your home at some point in the future—but not right now—will allow you to plan your remodeling projects with more time on your hands which could make it more financially feasible to complete them.

For more information on how you can prepare to sell your home, connect with one of our local agents—we’re always happy to chat about your situation and offer advice.

1©2021 Zonda Media, a Delaware corporation. Complete data from the 2021 Cost vs. Value Report can be downloaded free at www.costvsvalue.com.

This article originally appeared on the Windermere blog January 10, 2022. Written by: Sandy Dodge.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2022, Windermere Real Estate/Mercer Island.

Thinking About Buying a Second or Vacation Home?

Here are a few tips to make sure it’s worthwhile…

These days, having your own home away from home is a compelling concept. There are many clear benefits including being able to use your home how you wish, decorate to your taste, and include your furry friends in your time away. There are also challenges to be considered as home security, maintenance, and holding expenses are nothing to ignore.

One consideration to start with is whether the home will be solely used by your family or become an income-producing vacation rental. In addition to being a lifestyle choice, this determination will impact your income taxes and insurance needs and should be made before you embark upon this journey.

There are advantages and disadvantages to both options:

Owning as a Personal Second Home

PROS

- Comfort: Returning to the same place is familiar and often more relaxing than staying in a hotel or vacation rental. It allows you to enjoy your space as you wish and include pets and hobbies in your home away from home. Proximity to your primary residence is an important factor. How long will it take to get there? You will likely visit more often if your second home takes under three hours to travel to. Choosing a location that you will enjoy for years to come is essential to making a good purchase decision.

- Convenience: The ability to keep your possessions that are used exclusively at the second home simplifies travel and packing and makes it easier to be surrounded by the things you enjoy.

- Long-term profit: While assets fluctuate in value in the short term, vacation properties are more likely to retain their value and appreciate because they are located in popular areas with a geographically limited supply. At some point you could have a nice nest egg or a property that becomes a family vacation home for future generations.

- Future retirement options: A common retirement goal is to have a place to retreat for part of the year in addition to your main residence. Whether a second home will become a full-time venue in retirement or continue to be a part-time get-away, having it established before retirement gives you options.

CONS

- Initial cost: Buying a second or vacation home is a big investment. Down payment requirements are typically higher on non-primary residences and that cash outlay can take away from other investment opportunities.

- Maintenance: Your second or vacation home will require maintenance and upkeep just like your primary residence. You’ll need to plan to tackle that yourself or hire someone else to do it for you. Let it get away from you, and you will be spending your leisure time worrying about everything that needs to get done instead of relaxing.

- Commitment: When you are paying a significant amount of money each month for a second or vacation home, you may feel that you need to constantly visit the property to justify your investment. You’ll need to ask yourself if the idea of going to the same place over and over again is appealing or a turn-off.

- Other considerations: Evaluating and mitigating your exposure to natural disaster (fire, flood, earthquake, tsunami, etc.) and liability risks (guest injury, burglary, squatting, vandalism, arson) on a home that is vacant for much of the time is an important consideration. Determine how you will keep your home safe and secure.

Owning as an Income-Producing Vacation Rental

PROS

- Income to offset expenses: A good vacation rental property generally provides a healthy rental revenue which could potentially cover mortgage payments and operating expenses. Using an online short-term rental service like Airbnb makes it convenient to manage your rental property. Their website interface makes pricing, marketing, and communication with potential guests straightforward and easy. Airbnb will also oversee the billing process for you.

- Tax considerations: You may qualify for federal tax breaks and deductions related to holding your investment property. This can help offset the expense of owning and provide investment opportunities for the future.

- Long-term profit: Like a second home, vacation properties are more likely to retain their value and appreciate over time. At some point you could have a nice nest egg or a property that becomes a family vacation home for future generations.

- Future retirement options: While there are tax considerations to converting an income-producing property into a personal use property, owning a vacation home allows you to insulate yourself against rising real estate prices and give you options for future use.

CONS

- Initial cost: Buying a vacation home as an investment property will require both a hefty down payment and initial start-up expenses to furnish and supply the home. You will need to evaluate that cash outlay with other potential investment opportunities.

- Management and maintenance: Vacation rentals can be costly to manage, both in terms of time and money. These properties may require seasonal upkeep and special maintenance considerations. You may even incur costs to maintain or monitor the property even when it’s not actively being utilized.

- Revenue fluctuations: Vacation rental properties are particularly sensitive to seasonal fluctuations and economic downturns, which could leave you financially exposed. Having a property that is attractive in multiple seasons is a definite plus.

- Short-term rental restrictions: Many state and local municipalities are seeking to reign in short-term vacation rentals, which could put a damper on potential revenue from these properties. Many now require a minimum rental period of 30 days. In contrast, there are locations that are ideal for these kinds of short-term rentals. Look into regional ordinances, do a Google search, and check out local newspapers to discover recent talk of changing or enforcing such codes.

- Other considerations: In addition to evaluating and mitigating your exposure to natural disaster and liability risks, you will want to consider other holding expenses. These might include higher renovation and repair costs due to high-use or damage. Most travelers expect the latest appliances and furnishings, so you will have to update every few years. Unfortunately, short-term renters are less likely to report any necessary repairs and guests are far less likely to treat the property with respect since there is no sense of ownership or obligation.

Final Thoughts

Regardless of your decision to use the property personally or as an investment, checking in with your CPA and financial advisor is a good first step. They can advise you of pros and cons of each approach, States that are more or less favorable to own a non-primary residence in, and whether you should establish a trust or LLC to hold the property in.

Having a savvy real estate broker help you understand the local scene, evaluate options, and provide vetted resources is essential, especially when you are looking in an area you are less familiar with.

Still have questions? Conact me for assistance with exploring a second and vacation home purchase locally, or I can refer you to a great broker in other areas you are considering.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2021 Windermere Mercer Island

Payback times for energy-efficient home upgrades

Thinking of going green? Today’s technology offers a whole host of ways to boost your home’s efficiency, reduce your carbon footprint and lower your energy bills. Some upgrades can pay for themselves in a relatively short amount of time, while others with large price tags might take decades to start paying back. The good news is that several studies have shown buyers are willing to pay a premium for green features—as much as 30% more for retrofitted green homes that become Energy Star or LEED-certified. This means that even if those fancy new features don’t pay you back right away in energy savings, you might still be able to recoup part of the cost when you sell your home. Below are the average payback times for some common items…just keep in mind that the actual payback time will depend on your initial costs and the amount of energy you typically use each month.

According to EnergySage.com, the average cost for adding solar panels to your home in King County is about $13,850 for a typical 5kW system (a net cost of $10,249 after the 26% Federal Investment Tax Credit for 2020). Based on the amount of energy they generate in our area, they usually pay for themselves in about 10.16 years. Furthermore, a study commissioned by the Department of Energy found that home buyers across multiple states and home types were willing to pay more for homes with solar panels (about $15,000 for homes with a 3.6kW system). This may help offset your costs should you need to sell your home before the payback period.

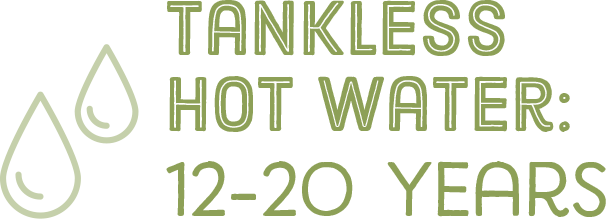

In addition to giving you endless hot water, tankless water heaters are also about 20% more energy efficient than traditional storage tanks and last about 10 years longer. However, their additional equipment and installation cost means it can take quite a while for your energy savings to cover that difference—12-20 years for electric models and 22.5-27.5 years for gas models. Their longer lifespan may ultimately help them pay off in the long run.

Looking for an easy investment with quick bang for your buck? LED bulbs may cost more, but the amount of electricity they save more than covers the cost. A 100W equivalent LED bulb costs about $6 to buy but uses only 13% the amount of energy of its incandescent counterpart. Used 4 hours a day, it also reduces CO2 emissions by a whopping 262.93 pounds per year. Depending on the number of bulbs you have and the frequency of their use, the dollar and carbon savings could really add up over time.

Our Seattle area’s temperate climate makes it a prime candidate for heat pump heating/cooling systems. Your actual savings and payback time will depend on the type of system you choose and the amount of energy you use. According to the US Department of Energy, an air source heat pump can reduce your electricity use for heating by about 50%, while the reduction range for a geothermal heat pump is anywhere from 30%-60%. If you’re also replacing an A/C unit, the savings will add up even faster. The average installed cost in 2020 is about $5,613 nationally but can vary quite a bit; it pays to do your research and make sure you’re choosing the right unit for your needs. Boosting your home’s overall efficiency first can also increase your savings by allowing you to choose a smaller, more affordable unit.

A feature of most modern green homes, smart thermostats save energy by automatically turning off the heating and A/C when you leave and learning your schedule to comfortably boost efficiency. Nest estimates an average yearly energy savings of 10-15% or $131-$145 with its Learning Thermostat, which means it would pay back its $200-$250 price tag in under 2 years. The ecobee4 is pricier at $300-$400 but claims to save 23% on heating and cooling (or more if you use their free eco+ upgrade). With heating and cooling making up a large chunk of your household energy use, smart thermostats could potentially take a nice chunk out of your carbon footprint as well.

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

© Copyright 2020, Windermere Real Estate / Mercer Island